Executive Summary

The following report is an overview of SunTrust’s progress under the National Mortgage Settlement (NMS or Settlement).

This report includes a review of SunTrust’s compliance with the Settlement’s servicing standards for the first half of 2017.

I have reviewed SunTrust’s internal review group’s (IRG) compliance metric testing results and concluded that SunTrust did not fail any of the compliance metrics. I have also determined, based on further work that I required SunTrust to undertake, that SunTrust failed Metric 4 in each of the four quarters of 2016.

I will continue to monitor and report on SunTrust’s compliance with the servicing standards.

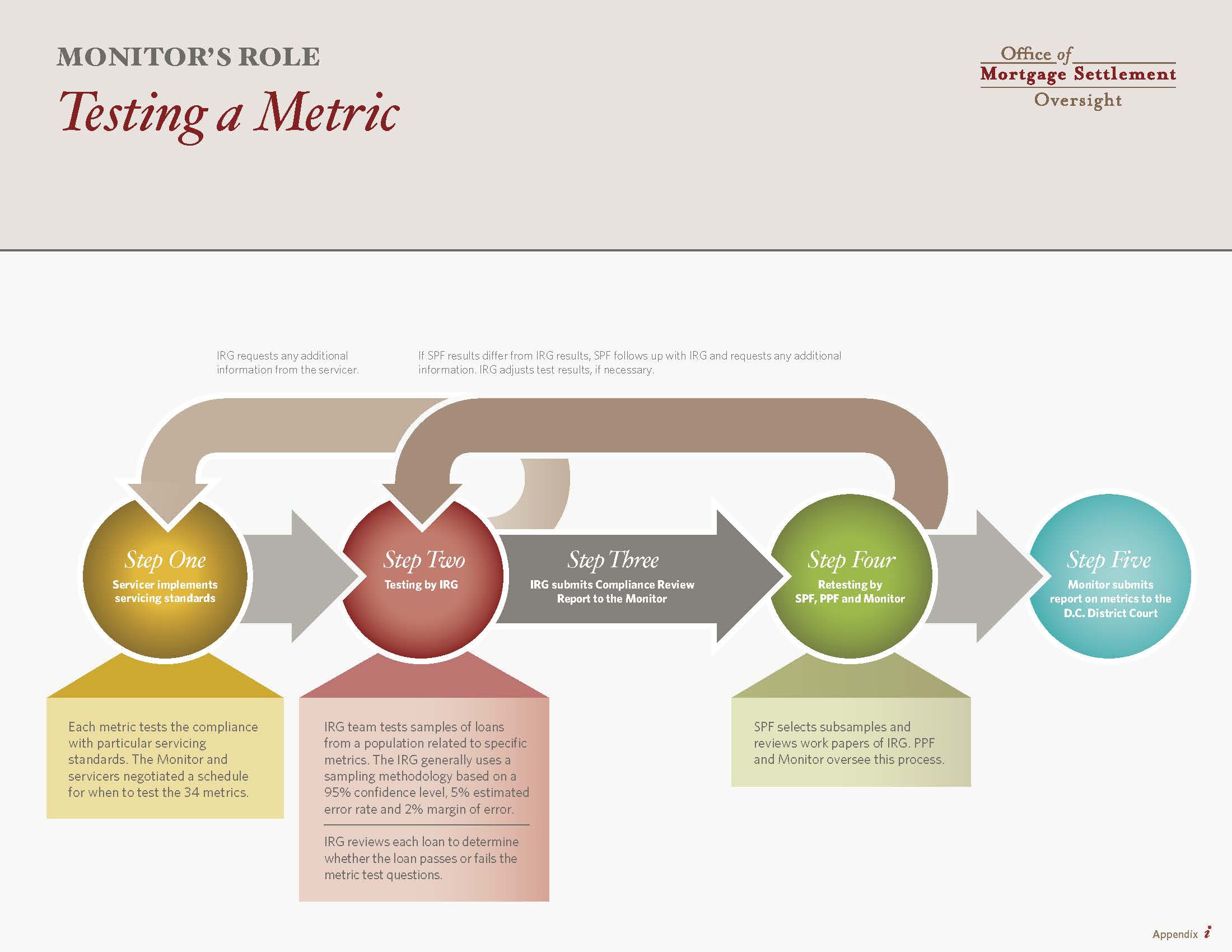

To evaluate SunTrust, I work with a team of professionals. SunTrust followed a work plan in which the IRG determined whether the servicer complied with the Settlement terms. My professionals and I then reviewed the work of the IRG. I determined that the IRG’s work was satisfactory and reported my findings to the Court and the public. For more information about the oversight and review process, please see my previous reports.

Sincerely,

Joseph A. Smith, Jr.

Servicing Standards Compliance

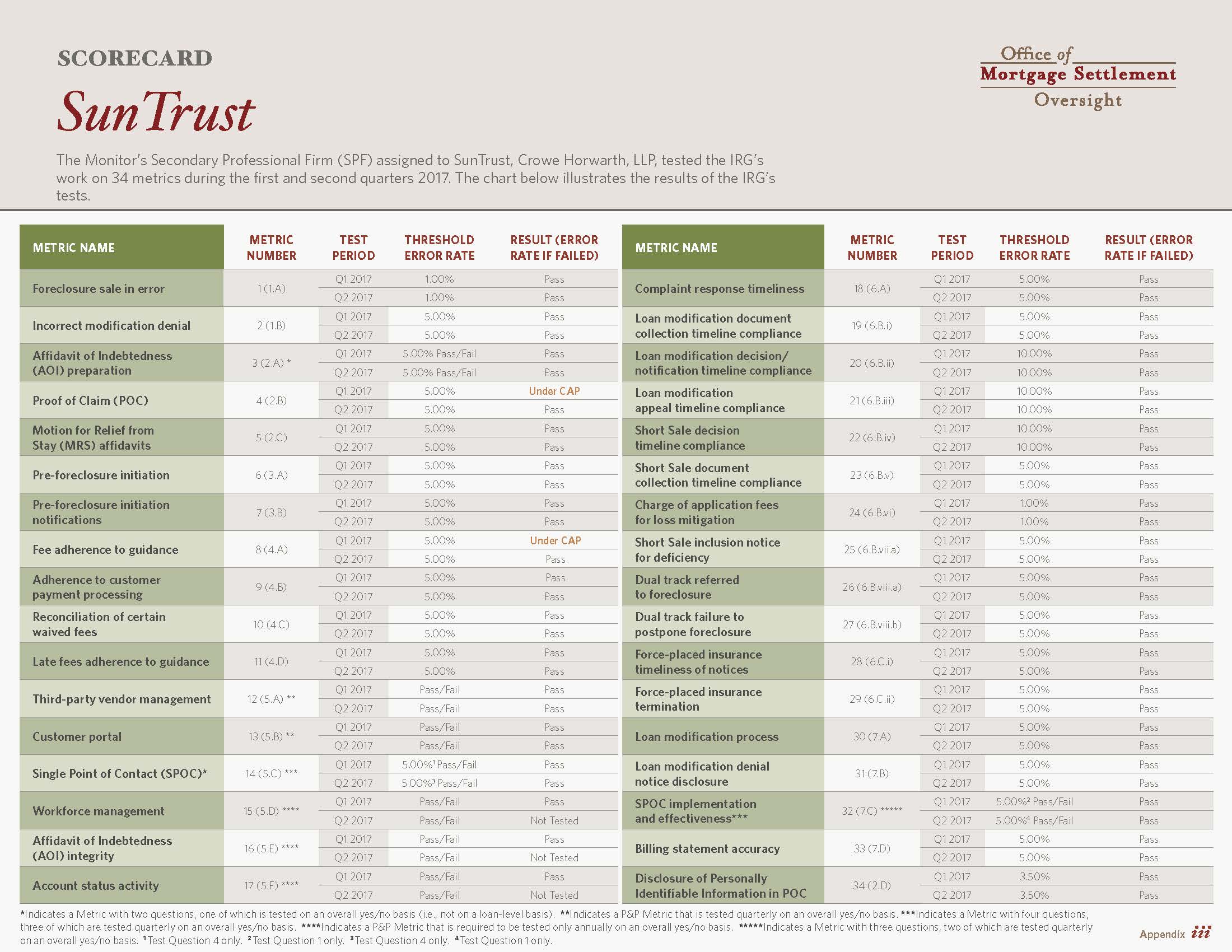

I evaluated SunTrust’s compliance with the Settlement’s servicing standards using the 34 metrics, or tests, enumerated in the Settlement.

These metrics determine whether SunTrust adhered to the 304 servicing standards, or rules, contained in the NMS. The work to test SunTrust in the first and second quarters of 2017 involved 37 professionals, including my primary professional firm, secondary professional firm and other professionals who dedicated approximately 15,495 hours.

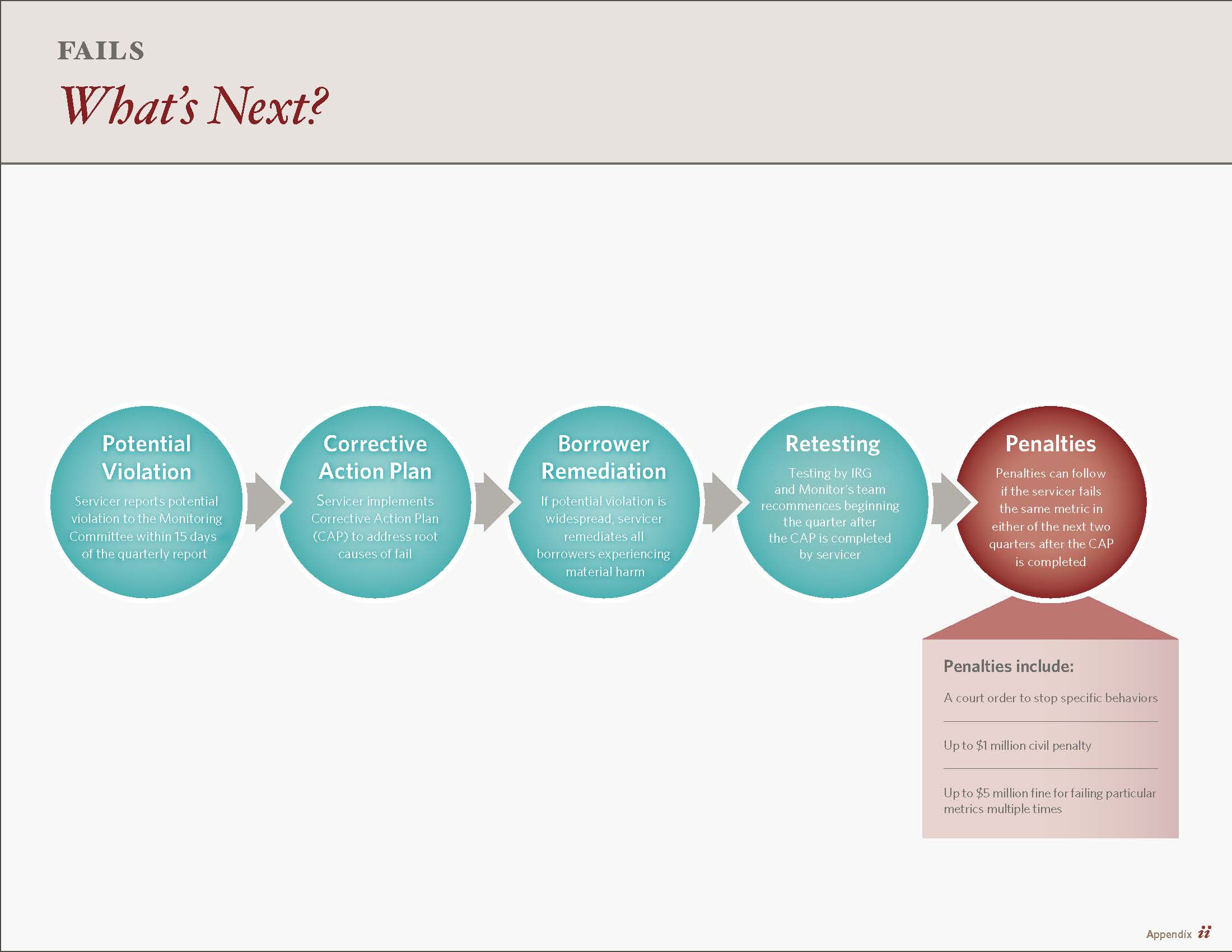

This report covers the first and second quarters of 2017, and I tested SunTrust on all 34 metrics. The NMS defines a failed metric as a potential violation and gives the servicer a chance to fix the root causes of its failure. For more information on what happens when a servicer fails a metric, see the graphic in Appendix ii. I also included information on metric fails and corrective action plans (CAPs) in my previous reports.

Update on SunTrust's Corrective Actions

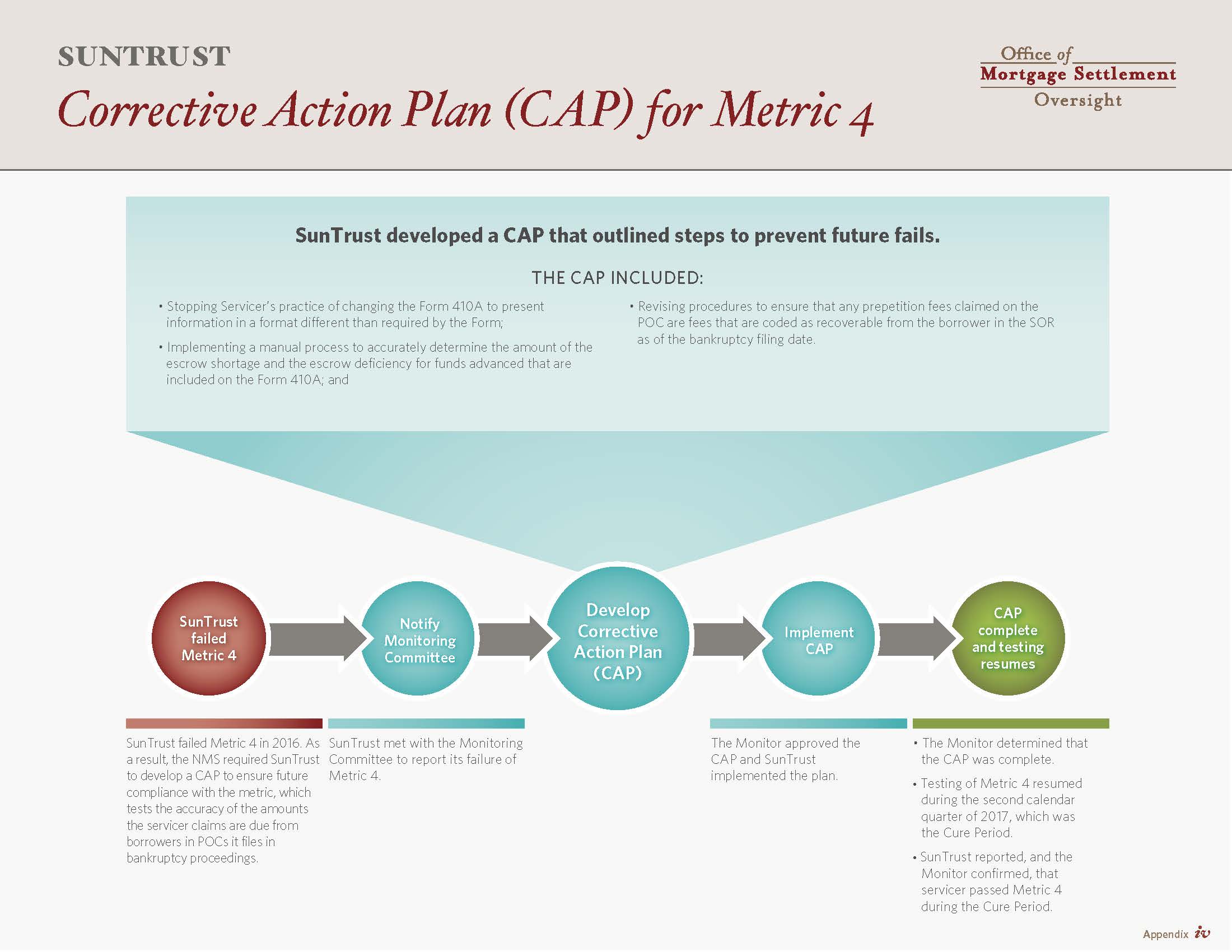

Metric 4

This metric tests the accuracy of information on Proof of Claims (POCs) filed in Bankruptcy Court. As I noted in my prior report, I rejected SunTrust’s test results for Metric 4 in the fourth quarter of 2015 and all four quarters of 2016 because SunTrust had changed official Bankruptcy Form 410A (the Mortgage Proof of Claim Attachment) to provide information differently than contemplated by the official form.

I required SunTrust to perform an analysis of all POCs filed from December 2015 through January 2017 to correct the Form 410A and determine whether there were differences in the original incorrectly prepared form and the corrected form. The results of this analysis showed that SunTrust had exceeded the Threshold Error Rate for Metric 4 in all four calendar quarters of 2016, and that the failure was widespread in each of those quarters.

SunTrust submitted its proposed Corrective Action Plan (CAP) in September 2017. My professionals and I reviewed and I approved SunTrust’s CAP. I also determined that SunTrust had satisfactorily implemented the CAP as of April 1, 2017. Testing resumed during Q2 2017, which was the cure period. SunTrust reported and I confirmed that servicer passed Metric 4 during the cure period.

Remediation

Because the failure was widespread, I required SunTrust to identify and remediate all potential borrower harm. SunTrust filed amended POCs in all active bankruptcies where the errors on the original, incorrectly prepared forms were greater than one dollar. In addition, SunTrust identified all borrowers for whom SunTrust had collected more than the borrower actually owed based on the corrected forms and SunTrust made refunds to the appropriate parties.

Finally, for those borrowers who were no longer active in bankruptcy, I required SunTrust to mail letters to the borrowers and the bankruptcy Trustees informing them of the errors in the original forms and providing the borrowers the opportunity to contact SunTrust if the borrower suffered any damage as a result of the errors.

SunTrust is continuing to implement aspects of the remediation plan related to this metric. I expect SunTrust to complete the plan soon, and I will report on SunTrust’s progress in future reports.

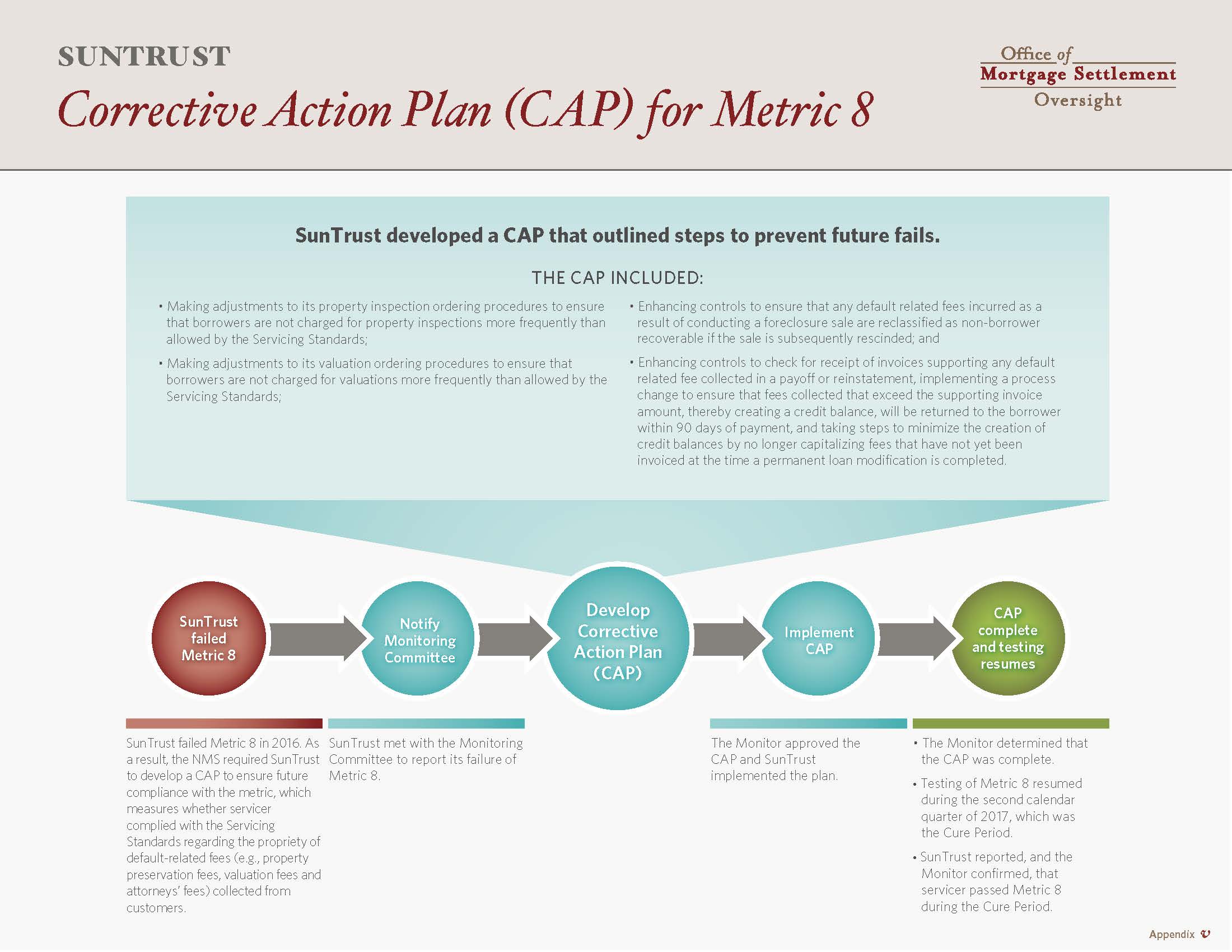

Metric 8

This metric tests whether SunTrust properly collected default-related fees from borrowers. Those fees include property preservation fees, valuation fees, and attorneys’ fees.

I approved SunTrust’s Corrective Action Plan in February 2017. My professionals and I reviewed and determined SunTrust’s CAP and remediation was completed in April 2017. SunTrust reported and I confirmed the servicer passed Metric 8 during the cure period, which was the second quarter of 2017.

Conclusion

SunTrust continues to make progress under the NMS. I will continue to monitor SunTrust’s compliance with the Servicing Standards and will report on my review of the next two testing periods to the Court and the public early in 2018.